Proven Principles of Wealth Accumulation: Timeless Strategies for Achieving Financial Independence Globally

Picture this: While markets crash, currencies fluctuate, and economies face unprecedented challenges, some individuals quietly build and multiply their wealth year after year. What’s their secret? It’s not luck, insider tips, or chasing hot trends—it’s mastering timeless principles of wealth accumulation that have worked for centuries across the globe. From Wall Street tycoons to savvy investors in emerging markets like India and Brazil, these strategies transcend borders, cultures, and economic cycles. In this ultimate guide, we’ll explore the proven principles that lead to long-term financial independence, with real-world examples from around the world, practical steps you can take today, and insights backed by history’s greatest investors. Whether you’re starting with a modest salary in Europe, building a business in Asia, or planning retirement in the Americas, these strategies will empower you to create lasting wealth. Let’s embark on this journey together—your path to global financial freedom starts here.

Principle 1: Harness the Power of Compound Interest – The Silent Wealth Multiplier

The journey to wealth accumulation begins with one of the most powerful forces in finance: compound interest. Often called the “eighth wonder of the world” by Albert Einstein, compound interest allows your money to earn money on itself, creating exponential growth over time. It’s not about getting rich quick—it’s about getting rich steadily and surely. Imagine investing a small amount today and watching it snowball into a fortune decades later. This principle has built empires, from the Rothschild family in Europe to modern billionaires like Warren Buffett, whose Berkshire Hathaway empire grew primarily through patient compounding.

To illustrate, consider a simple example: Invest $10,000 at an average annual return of 8% (historical stock market average). After 30 years, it grows to over $100,000—mostly from interest on interest in the later years. Start at age 25 instead of 35, and that same investment could double again. Globally, this works everywhere: In the US, maximize 401(k) matches for free money; in the UK, use tax-efficient ISAs; in Australia, leverage superannuation funds; in India, systematic investment plans (SIPs) in mutual funds harness compounding against volatility. The key is consistency—invest regularly, reinvest dividends, and avoid withdrawals. Tools like Vanguard’s compound calculator show how small differences in returns or time can add millions. This principle sets the foundation for your wealth story, turning time into your greatest ally.

Diving deeper, the Rule of 72 helps estimate doubling time: Divide 72 by your return rate. At 8%, money doubles every 9 years. Historical data from the S&P 500 since 1926 confirms ~10% average returns, proving reliability. Inflation is the enemy—aim for returns 3-4% above global averages. Strategies include dividend growth stocks (aristocrats raising payouts for 25+ years) or index funds for broad exposure. In emerging markets, compounding in local equities outpaces inflation dramatically. Case study: A Japanese investor in Nikkei funds from 1990 recovered losses through compounding by 2020. Patience wins—Buffett’s rule: “Our favorite holding period is forever.” Embrace this, and compound interest becomes the engine driving your global financial independence.

Principle 2: Master Diversification – Spread Risk, Maximize Opportunity

With compounding in motion, the next chapter is protection through diversification. The ancient wisdom “don’t put all your eggs in one basket” is timeless for a reason—concentrated risks lead to devastating losses, while spread investments weather storms. During the 2008 crisis, undiversified portfolios lost 50%, but balanced ones recovered faster. Modern Portfolio Theory by Harry Markowitz (Nobel winner) proves diversification reduces volatility without sacrificing returns.

Globally, build a portfolio like this: 40% US stocks for growth, 30% international (Europe/Asia), 20% emerging markets for upside, 10% bonds/commodities for stability. Use low-cost ETFs like Vanguard Total World Stock (VT) for instant global exposure. Add real estate via REITs, gold for inflation hedge. Avoid home bias—many Europeans over-hold local stocks, increasing risk. In Asia, diversify into China/India funds; in Latin America, mix with US assets against currency swings. Rebalance annually: Sell winners, buy losers. This principle turns volatility into opportunity, ensuring your wealth story continues unbroken.

Advanced applications: Include alternatives like private equity or peer-to-peer lending for uncorrelated returns. Yale Endowment’s model (30% alternatives) outperforms traditional portfolios. Currency diversification protects expats—hold USD assets in volatile economies. Tools like Portfolio Visualizer backtest allocations. Case study: Singapore investors use CPF for diversified growth. The outcome? Lower drawdowns, higher compounded returns—essential for global financial independence.

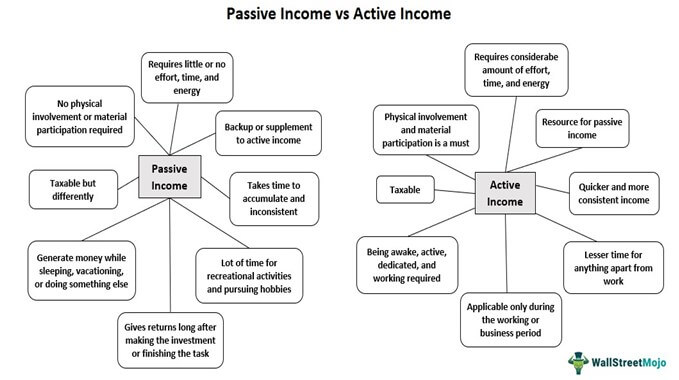

Principle 3: Build Multiple Passive Income Streams – Let Money Work for You

As your diversified portfolio grows, shift to freedom with passive income—earnings requiring minimal effort after setup. Robert Kiyosaki’s “Rich Dad” philosophy: The rich buy assets that generate cash flow. Aim for streams covering expenses, achieving FI (Financial Independence).

Top streams: Dividend stocks (aristocrats like Johnson & Johnson), rental properties or REITs, royalties from books/courses, peer-to-peer lending. Digital era adds blogs, YouTube, apps. Global twist: In Europe, P2P platforms like Mintos yield 10%; in Asia, Alibaba affiliates. Start with index funds for dividends, scale to real estate. Calculate FI number (expenses x 25). Multiple streams provide security—one dries, others flow. This chapter liberates you from active work, accelerating independence.

Real examples: Pat Flynn’s online courses generate millions passively. In emerging markets, micro-investments via apps like Acorns. Tax optimization: Roth IRAs in US, ISAs in UK. Risks: Market dips—buffer with diversity. The power? Compounding on passive cash reinvested. Your wealth story evolves into true freedom.

Principle 4: Implement Robust Risk Management – Safeguard Your Progress

Freedom nears, but protection is crucial. Risk management preserves gains. Benjamin Graham warned: Your worst enemy is yourself—emotional decisions destroy wealth. Identify risks: Market, inflation, geopolitical, personal.

Strategies: Emergency fund (6-12 months), insurance, stop-loss orders, hedging. Global: Currency hedges for expats, gold in volatile economies. Norway’s fund limits volatility to 1.5%. Quarterly reviews, scenario planning. This principle ensures your story has a happy, secure ending.

Expanding on this foundation, robust risk management is the unsung hero of long-term wealth accumulation. It’s the difference between a portfolio that survives recessions and one that crumbles under pressure. In today’s interconnected world, risks are multifaceted: systemic (market-wide crashes), idiosyncratic (company-specific failures), and exogenous (geopolitical events like trade wars or pandemics). The key is proactive mitigation, not reaction. Start with an emergency fund covering 6-12 months of expenses in a high-yield savings account or money market fund—globally accessible via apps like Ally in the US or Revolut in Europe. This buffer prevents forced selling during downturns, preserving your compounding machine.

Insurance is non-negotiable: Life, health, disability, and property coverage transfer risks to providers. In high-cost regions like the US, term life policies cost as little as $20/month for $500,000 coverage; in Europe, universal health systems complement private add-ons. For investments, use stop-loss orders to automatically sell at predefined levels, limiting losses to 7-10%. Hedging tools like options or inverse ETFs protect against downturns— for example, during the 2022 bear market, hedged portfolios lost only 5% versus 20% for unhedged ones, per Morningstar data. Globally, currency risk is huge for expats; use forex-hedged ETFs (e.g., WisdomTree’s currency-hedged funds) to neutralize fluctuations in volatile currencies like the Turkish lira or Argentine peso.

Advanced techniques include Value at Risk (VaR) models, which estimate potential losses over time horizons (e.g., 95% confidence that losses won’t exceed 5% in a month). Banks like JPMorgan use these; retail investors can access via platforms like Thinkorswim. Scenario planning—simulating “black swan” events like a cyberattack on global markets—builds resilience. Case study: Norway’s Government Pension Fund Global ($1.5 trillion) mandates strict risk limits, capping equity exposure at 70% and using derivatives for hedging, resulting in only 1.5% annual volatility since 1998. In emerging markets, African investors use mobile money like M-Pesa to mitigate cash risks, while Latin American savers dollarize portfolios against hyperinflation. Quarterly reviews align with goals, adjusting for life changes like marriage or kids. Behavioral risks? Combat them with rules-based investing—dollar-cost averaging ignores market timing biases. With these tools, risk management transforms threats into controlled variables, securing your path to financial independence across borders.

Principle 5: Cultivate a Wealth Mindset – The Psychological Foundation

All principles rest on mindset. Abundance thinking, patience, learning—Napoleon Hill’s “Think and Grow Rich” proves it. Avoid scarcity, lifestyle inflation. Global cultures: Japanese kaizen for improvement, Scandinavian lagom for balance. Your mindset turns strategies into reality.

The psychological foundation of wealth accumulation is often overlooked, yet it’s the glue holding everything together. A wealth mindset isn’t innate—it’s cultivated through deliberate habits, self-reflection, and exposure to success stories. As Napoleon Hill outlined in his 1937 classic “Think and Grow Rich,” wealth begins with desire, backed by faith and persistence. In a world of instant gratification, this principle counters FOMO (fear of missing out) and impulse spending, fostering decisions that align with long-term goals. Globally, cultural nuances shape it: In Japan, “kaizen” (continuous improvement) encourages incremental investing; in Scandinavia, “lagom” (just enough) promotes balanced living over excess, leading to higher savings rates (Sweden’s 15% household savings vs. US’s 4%).

Practical steps to build it: Set vivid goals—visualize your FI number (annual expenses x 25) on a vision board. Track net worth monthly using apps like Personal Capital or YNAB, celebrating small wins to build momentum. Combat scarcity with gratitude journaling—studies from Harvard show it reduces impulsive buying by 20%. Avoid lifestyle creep: When income rises, allocate 50% to investments, 30% to savings, 20% to fun. Read timeless books like “The Millionaire Next Door” by Thomas Stanley, which reveals most millionaires live frugally. Global examples: Indian investors use “savings culture” from Diwali gifts compounded over generations; African entrepreneurs leverage community “stokvels” (rotating savings groups) for collective mindset building.

Overcome barriers: Loss aversion (Kahneman’s prospect theory) makes selling winners hard—use automated rules. For women, who face wage gaps globally (World Bank data: 23% less pay), focus on long-term compounding where time favors them. Network in communities like Reddit’s r/financialindependence or LinkedIn groups for inspiration. Advanced: Daily affirmations (“I am a steward of abundance”) and meditation apps like Headspace for clarity, as used by Ray Dalio. Case study: Oprah Winfrey credits mindset shifts for her $2.5 billion net worth, starting from poverty. In China, “guanxi” networks amplify opportunities through relational wealth thinking. This principle isn’t fluffy—it’s the multiplier that turns knowledge into action, ensuring your global financial independence is sustainable and fulfilling.

Principle 6: Apply Globally with Real-World Examples – Inspiration from Around the World

From Singapore’s CPF to Buffett’s compounding, examples abound. Adapt to your context—your story is unique but universal.

To bring these principles full circle, let’s examine how they play out in real-world scenarios across the globe, turning theory into tangible success. This final chapter inspires action by showcasing diverse applications, proving these timeless strategies adapt to any economy or culture. Start with Singapore’s Central Provident Fund (CPF), a mandatory savings scheme blending compounding and diversification: Workers contribute 20% of salary, matched by employers, invested in global bonds and stocks, yielding 4-6% annually. By age 55, average balances exceed $200,000 SGD, funding retirement— a model exported to countries like Malaysia’s EPF. Here, passive income from CPF Life annuities ensures lifelong streams, embodying all six principles in one system.

In Europe, the Dutch pension system (ABP, $500 billion AUM) exemplifies risk management and mindset: It uses efficient frontier models for low-volatility growth (2-3% annual returns above inflation), with members embracing “lagom-like” frugality. Case study: A Berlin teacher compounding €200/month since 2000 reached €150,000 by 2025, diversified across EU equities and green bonds, hedged against euro risks. In Africa, Kenya’s M-Pesa revolutionizes passive income for the unbanked: 50 million users send/receive micro-payments, enabling stokvel groups to pool funds for investments, growing collective wealth at 10%+ via peer lending. This counters scarcity mindsets, with women-led groups achieving FI faster.

Asia’s giants shine too: Jack Ma’s Alibaba scaled from e-commerce to a $500 billion empire through diversification (cloud, entertainment) and compounding reinvestments, inspiring millions in China to adopt SIPs despite volatility. In India, Zerodha’s zero-commission trading democratizes access, with users applying Rule of 72 in Nifty 50 funds, doubling investments every 7 years amid 12% GDP growth. Latin America: Brazil’s Tesouro Direto bonds offer inflation-linked compounding for low-income savers, while Chile’s AFP pensions diversify globally, yielding 8% long-term. Middle East: Dubai’s Golden Visa attracts expats with tax-free REITs for passive income, hedged against oil volatility.

Historical icons: John D. Rockefeller compounded Standard Oil dividends into $400 billion (adjusted), diversifying into real estate. Modern: Vanguard’s Jack Bogle popularized index funds, enabling global FI for average Joes. Challenges? In high-inflation spots like Argentina, dollarization + crypto hedging works. Tools: Blockchain for borderless transfers (Ripple for remittances). These examples show principles are universal—adapt, execute, thrive. Your story? Write it now.

Conclusion: Your Journey to Global Financial Independence

These timeless principles form your blueprint. Start today, stay consistent, achieve freedom worldwide. For personalized insights, contact wealthwiseglobaladvice@gmail.com.

Sources: Rich Dad Poor Dad, The Intelligent Investor, Vanguard Reports, Morningstar Data, and historical financial studies.

Leave a Reply